GAP Under Attack

September 16, 2020

By: Michael J. Dommermuth and J. Randolph Earnest

The Colorado Attorney General launched a significant investigation into GAP practices in Colorado. Subpoenas were served on multiple GAP administrators seeking a broad range of documents and information concerning GAP.

In addition, at least ten GAP class action lawsuits were recently filed in Colorado. The GAP Class Action lawsuits were only filed against finance companies and allege failure to make refunds of unearned GAP fees after cancellation/termination.

The current regulatory actions and class actions appear to be focused on refunds. Typically GAP refunds are handled through the dealer that sold the GAP. If you receive a GAP refund for a consumer, you are responsible to add the dealer’s pro rata portion of the GAP premium and refund the total refund amount to the consumer. If the dealer cannot locate the consumer to make the refund, the funds should be turned over to the State of Colorado, as unclaimed property. Every dealer should maintain meticulous records concerning refunds.

Dealers are not yet targeted in these legal challenges, but this is an excellent time for dealers to audit their GAP practices and procedures to make sure that they are adhering to Colorado’s GAP regulations and their contractual obligations to the GAP administrators. The key elements are summarized below.

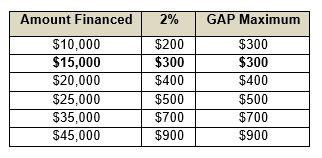

Colorado has strict caps on GAP charges. The GAP fee cannot exceed $300 or 2% of the amount financed, whichever is higher. The GAP fee limitations are summarized in the following table:

Colorado requires dealers to make written Bold Face disclosure to consumers:

- That the purchase of GAP is not required in order to obtain the credit or any particular or favorable credit terms;

- The fee of premium for GAP;

- That the consumer may wish to consult with an insurance agent to determine whether similar coverage may be obtained and at what cost;

- That GAP benefits may decrease over the term of the consumer credit sale or consumer loan;

- The consumer may cancel GAP for any reason, or no reason, within thirty (30) days after GAP was purchased and receive a full refund of the GAP fee or premium so long as no loss or event covered by GAP has occurred; and

- GAP is not a substitute for collision or property damage insurance.

In addition, the GAP contract must include the following statement:

“If this transaction contains a fee for or premium for guaranteed automobile protection, all holders and assignees of this consumer credit transaction are subject to all claims and defenses which the consumer could assert the original creditor resulting from the consumer’s purchase of guaranteed automobile protection.”

Colorado also requires that consumers be provided with a separate cancellation form at the time of contracting. This is something that the UCCC looks at during its routine audits. The cancellation form must include the following:

- The name and mailing address to be used to cancel GAP;

- State clearly and CONSPICUOUSLY that consumer has an unconditional right to cancel GAP for a full refund with thirty (30) days after it was purchased; and

- State that in order to cancel GAP, the consumer must complete and return the form or send any other written notice of cancellation to the address provided postmarked no later than thirty (30) days after GAP was purchased.